Is the 2026 Real Estate Market Headed for Change? Insights from History and Data

TL;DR

National housing crashes rarely play out like clockwork, regardless of cycle theories. Local market shocks and price corrections do occur, but the risk of a 2008-style crash in 2026 remains low. Instead, most experts see plateauing values, slower appreciation, and more negotiating room, especially in overheated regions.

Are We Facing a 2026 Real Estate Crash?

A contemporary living room that embodies current design trends and the evolving preferences of homeowners.

Despite warnings about an impending real estate crash in 2026, the likelihood of a major nationwide collapse is slim. While some local markets may experience notable corrections, housing market downturns are far more complex and regional than cyclical theories suggest. Recent data and expert insights point to a period marked by modest declines, lengthening listing times, and regionally divergent outcomes, rather than a dramatic crash reminiscent of 2008.

As buyers, sellers, and agents brace for the unknown, the question is not just whether a crisis is looming, but how evolving economic factors and real estate fundamentals may shape housing’s next chapter. Examining affordability, inventory trends, interest rates, and historic patterns reveals a story defined by nuance, not simple cycles.

-

Cycles, Myths, and the Reality of Housing Market Corrections

For decades, real estate observers have debated whether the industry moves in strict cycles, such as the so-called 18-year boom-and-bust pattern. In practice, these cycles rarely hold up to closer scrutiny. While 2008 stands out as a dramatic crash, earlier downturns (like those in the early 1990s and after the Dot-Com bubble) reflected different causes and timelines. As many industry veterans point out, downturns tend to arise from unique mixtures of economic shocks, lending standards, and shifting demand, rather than from any clockwork recurrence.

The current debate highlights the importance of perspective. In a forum conversation, users pointed out that regions like Pittsburgh sidestepped 2008’s worst effects, while cities such as New York saw moderate price adjustments. A homeowner in Boise described how, despite years of surging prices, mortgage payments now far exceed local incomes, making the possibility of a substantial correction real at the hyper-local level. Quantitative data from 2025 show only a 1-3% dip in home values for most major metros, lending weight to arguments that national declines are more likely to look like prolonged stagnation than widespread panic. Recent analysis of 2025 pricing trends reveals that modest price drops and slower sales are pressuring sellers and tempering expectations, but not leading to a destructive crash.

Expert Insight

A new homeowner in San Diego watched as the home next door was delisted after months without an offer, while another property down the street drew multiple cash offers the first weekend. It was a reminder that two blocks can be worlds apart in today’s market.

-

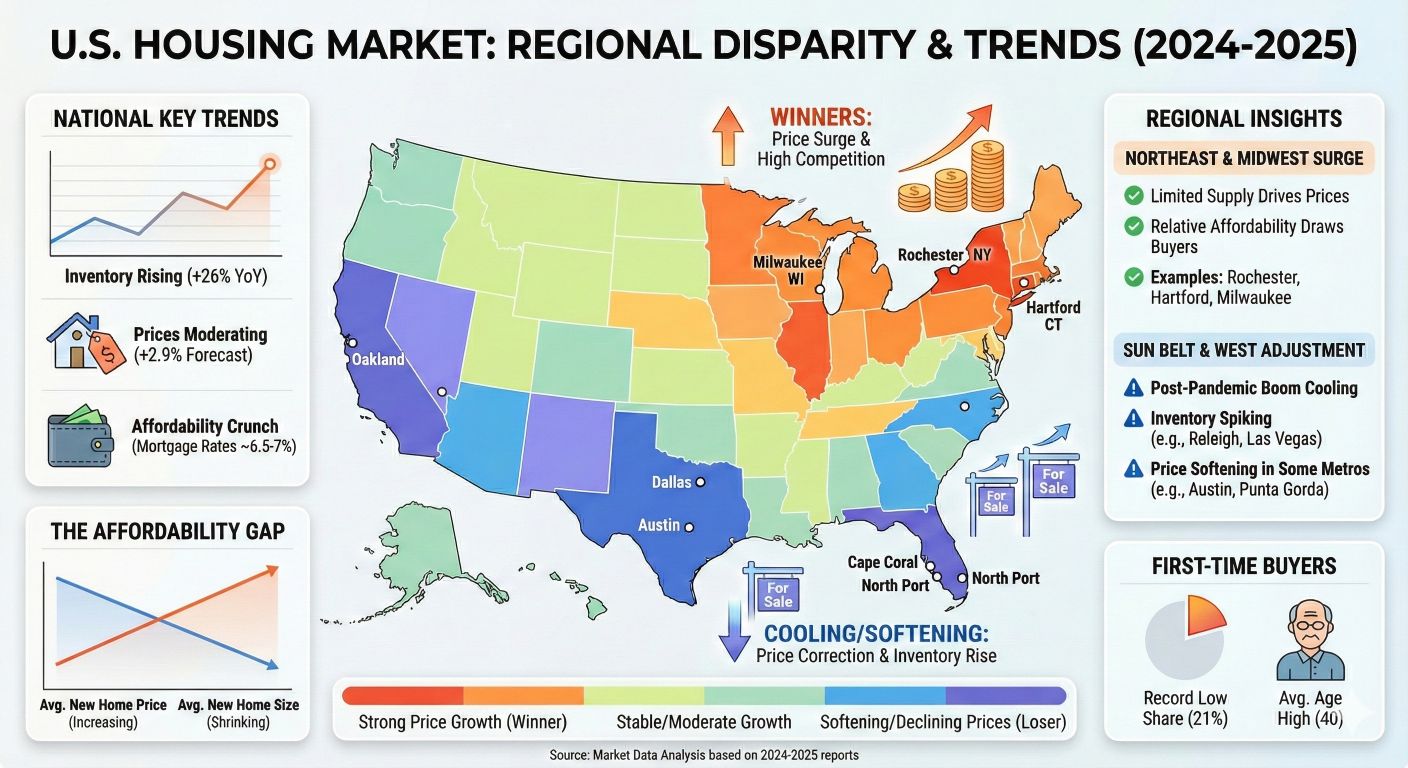

The Regional Divide: Winners, Losers, and Uneven Shocks

Analyzing the diverse impacts across U.S. housing markets: a visual guide to regional performance differences.

The most striking feature of recent housing market performance is the divergence between regions. Coastal cities like San Francisco and Los Angeles, influenced by high local incomes and international investment, continue to skew the national median home price upward. Meanwhile, the Midwest and much of the South tell a different story. In one illustrative scenario, a couple searching for a home in Kansas City in 2025 discovers that while home prices have plateaued, affordability remains within reach, in sharp contrast to their friends in Miami, where sticker shock is the norm. Market cooling patterns show longer days-on-market and rising inventory in some metros, but stability in others.

Austin, Texas, serves as a case study for volatility. Buyers who purchased at the 2022 peak saw prices drop nearly 20% by 2025, with predictions of further price decreases in the coming year. Yet, markets such as Pittsburgh and parts of New England have remained surprisingly stable. Local job growth, migration trends, and even property tax policies play as much a role as national interest rates. One homeowner in Maryland reported that federal layoffs were having a clear local impact, an experience not mirrored in nearby states.

-

Affordability, Leverage, and Lending: What Shapes 2026 Risk?

Several factors differentiate today’s real estate risk profile from the years leading up to the 2008 crisis. While affordability gaps are real, many households today face home prices far beyond what their incomes would traditionally support, lenders have enforced stricter standards and lower risk tolerance for a decade. Current borrowing often requires higher credit scores and substantial down payments, closing off the kind of speculative risk that fueled the last crash. Some regional exceptions exist, especially where homes remain vacant or rental markets stagnate, but nationally, the risk of mass defaults remains low.

For example, families in Boise considering buying versus renting face the reality that mortgage payments, especially at higher rates, may exceed local market rents by a wide margin. In these cases, the decision to rent and save is increasingly rational, especially with expectations of further price corrections. As outlined in the discussion of supply gaps and investor pressure, constrained supply, legacy low-rate mortgages, and new construction bottlenecks create an environment that favors stability, or at least gradual change, over sudden collapse.

One sharp real-world scenario: A tech worker in Austin buys in 2022, loses her job in 2025, and finds the house is now worth less than her mortgage. Unlike 2008, however, foreclosures remain rare, as buyers typically had more equity and stricter loan terms. Instead, she may choose to rent out the property or wait out the lull, an option that wasn't as available in the last downturn.

-

What Could Go Wrong? The Limits of Optimism

While most experts agree a 2008-style crash is unlikely, that doesn’t mean real estate is insulated from shocks. Rising insurance costs, volatile property taxes, and regionally weak job markets could all tip the balance in local markets. If unemployment climbs or credit becomes scarce, even strong local markets could wobble. A landlord in Milwaukee noted soaring property taxes eroding the profits of investment properties, a factor that could lead to higher rents or force sales at a loss. Price corrections, especially in cities that saw double-digit gains during the pandemic, may persist for years, not months.

On the national level, slower price growth and more inventory mean buyers will regain some leverage, with some areas already seeing more negotiation room and selective price cuts. Forecasts for 2026 highlight the shift toward a buyer-friendlier environment, but the return of widespread distress sales remains remote.

-

Common Mistakes to Avoid in a Volatile Housing Market

- Relying on National Headlines Alone: National news often glosses over local dynamics. Buyers who focus only on broad trends risk missing hyper-local changes that can dramatically affect property values. Monitor neighborhood data and work with agents who understand your market.

- Assuming History Will Repeat: Expecting a repeat of the 2008 crisis can lead buyers or investors to miss new opportunities or to sit out the market for too long. Understand the specific drivers in your region, including lending standards and supply constraints.

- Ignoring Total Cost of Ownership: Focusing solely on home prices while underestimating rising insurance, tax, or maintenance costs can upend budgets. Always analyze the full cost, not just the sale price.

-

Expert Insights for 2026 Housing Market Navigators

Expert discussions in a dynamic seminar setting, emphasizing data-driven approaches in housing market navigation.

- Shift Toward Analysis, Not Assumptions: Experts recommend drilling into the data, days on market, inventory, price cuts, rather than relying on old cycle models to predict what will happen next.

- Leverage New Visualization Technology: AI-driven platforms such as ReimagineHome.ai are making it easier for buyers and sellers to visualize remodels, staging, or even hypothetical market changes, helping clients weigh their options visually and analytically.

- Benchmark Against Local Metrics: Comparing home prices to local income, rent, and supply trends offers better insight than using the national median.

-

How Visualization Is Shaping Modern Housing Decisions

Transforming home design decisions through innovative visualization tools, paving the way for modern buyers.

One of the more transformative trends in today’s market is the use of visualization tools. Buyers frustrated by an unpredictable market can now employ services like ReimagineHome.ai to simulate renovations, model staging, or even evaluate potential investments before making a commitment. Practical applications range from a family in Atlanta visually updating a fixer-upper in advance of an offer, to an investor in Phoenix evaluating how changes to curb appeal might impact value on a softening street.

These technologies, especially when paired with granular local data, are quickly becoming essential for those navigating a landscape where minor differences between homes or neighborhoods have oversized impacts on outcomes.

Visualization Scenario

Imagine a family in Atlanta sitting around their dining table, using a visualization app to explore potential renovations on a home they’re considering buying. They adjust layouts, swap paint colors, and instantly see projected values for each option, helping them decide if the investment is worthwhile before making an offer.

Frequently Asked Questions About Real Estate Crash Risks in 2026

- Are home values expected to plummet nationwide in 2026?

Experts anticipate regional price corrections and slower appreciation, not a wholesale collapse reminiscent of 2008. - Which local markets are most vulnerable to declines?

Markets that saw rapid pandemic-era gains, like Austin and parts of Florida, are at higher risk for corrections, while many Midwestern and Rust Belt cities remain more stable. - How should buyers approach the 2026 market?

Assess local trends, compare rents and ownership costs, and use visualization and data tools to make informed decisions. - Are stricter lending standards protecting today’s buyers?

Yes. Tighter lending and more robust financial requirements are limiting risk, making widespread defaults less likely.

A Market Defined by Local Forces, Not Simple Cycles

Rather than expecting a synchronized national collapse or runaway boom in 2026, homebuyers, sellers, and investors are facing a market where every move is defined by local employment, affordability, lending standards, and, increasingly, powerful visualization tools like ReimagineHome.ai. The real risk isn’t in repeating history or clinging to predictive cycles, but in ignoring the diverse, grounded realities shaping each metro area. Learning to navigate these complexities, armed with tools, data, and a healthy skepticism, remains the wisest path forward.